The Impact of USDC Depeg on Coinbase

Research and Market Insights

Mar 27, 2023

What is a Stablecoin?

A stablecoin is a digital asset pegged to the value of other assets (fiat, gold, other cryptocurrencies) and designed to address price volatility and the on/off-ramp in the digital asset market, backed by the 1-to-1 equivalence it represents. For example, a stablecoin issuer pegged to the U.S. dollar would reserve one dollar for each stablecoin it creates as a reserve. Customers can exchange one dollar for a dollar-denominated stablecoin, and customers can redeem one dollar for a dollar-denominated stablecoin. There are three main types of stablecoins currently available in the market, namely stablecoins with fiat currencies and treasury securities as collateral (e.g., USDC and USDT), stablecoins with digital assets as collateral (e.g., DAI), and algorithmic stablecoins (e.g., AMPL).

What is USDC?

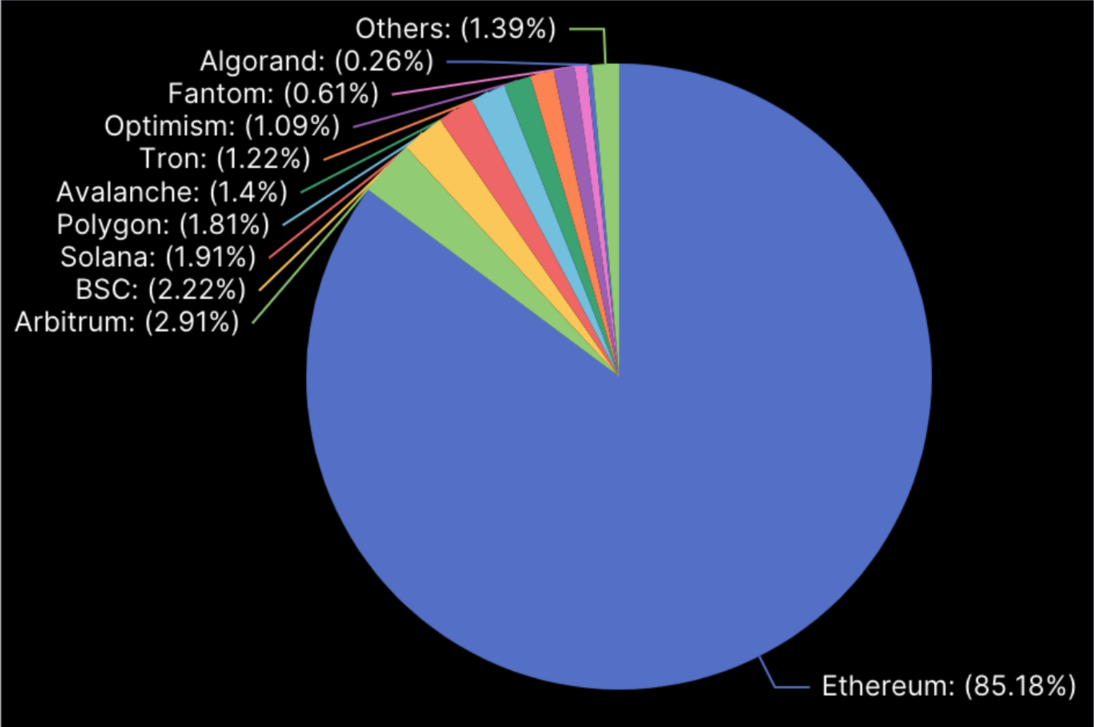

USDC is a stablecoin issued by blockchain payments technology company Circle in October 2018 that is pegged by fiat currencies and US Treasury bills as collateral in the US dollar and euro. The underlying technology behind it was developed by digital asset exchange Coinbase in partnership with Circle. Its circulating market capitalization had reached $56 billion at the peak of the bull market in 2021, and as of now (March 21, 2023), it has a circulating market capitalization of $36.9 billion, which is about 26.5% of the circulating market capitalization of all stablecoins. USDC is issued on multiple public blockchains, such as Ethereum, BSC, Solana, Polygon, etc., and on Ethereum the issue volume is $29.9 billion, accounting for 85% of the total issue volume.

USDC Issuance on Different Public Blockchains, Data source: https://defillama.com/

Since Defi Summer in 2020, USDC has quickly become the most trusted stablecoin in the Defi ecosystem, mainly because USDC is backed by Circle, which claims to have the most compliance licenses, and Coinbase, the world’s only NASDAQ-listed digital asset exchange. Circle has always been transparent and has begun to publish 100% of USDC’s reserves proof on its official website every month since 2018, the reserves include US dollars and short-term US Treasuries.

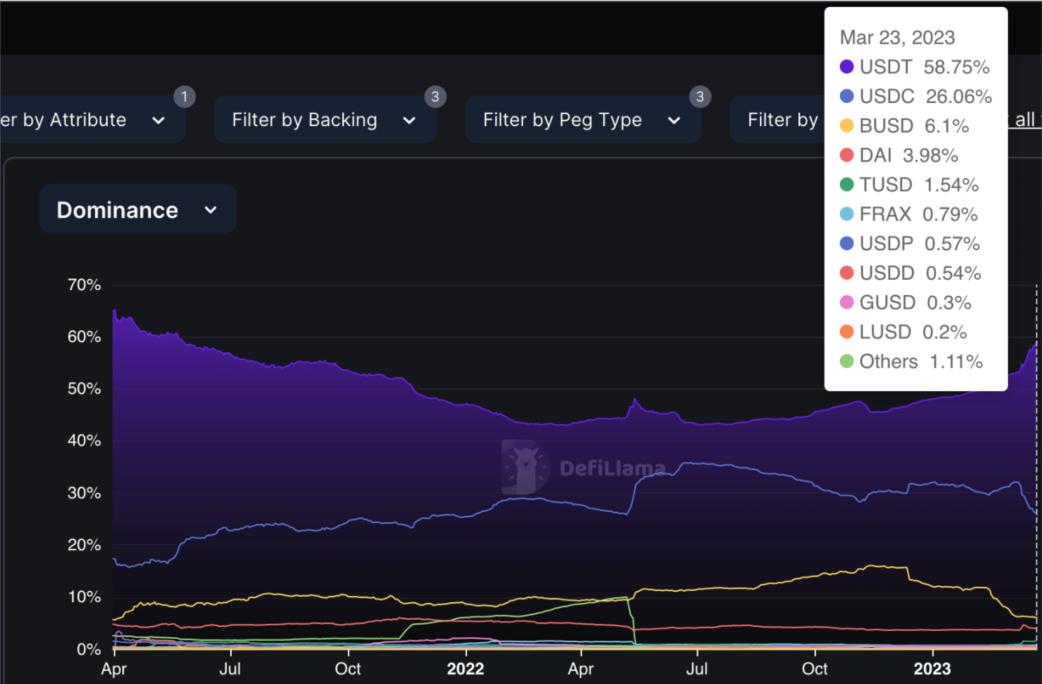

Percentage ofAllStablecoin Issues, Data source: https://defillama.com/

The revenue of a stablecoin issuer depends on the reserves and the rate of return on the reserves. Therefore, there are two ways for issuers to increase their revenue, raising reserves and increasing reserve yields. As long as the market demand for stablecoins increases, the stablecoin issuer can issue more stablecoins, and thus the reserve will increase accordingly. For the second approach, keeping every dollar in reserves ensures that dollars are always available (assuming the bank where the deposits are made does not fail), but the checking account generates almost no return. The lowest risk and most liquid assets are short-term U.S. Treasuries, such as 1-month and 3-month Treasuries.

Mechanism of USDC Mintingand Redemption

When a company deposits $1 into a specific Circle account, Circle will issue a $1 USDC to the user on a smart contract, which is the process of minting USDC. Likewise, when a company deposits $1 in USDC into the account, it can redeem $1, which is called redemption. The exchange is one of the users of USDC and when the exchange user redeems 1 USD for 1 USDC, the exchange generally provides USDC for the user to redeem. Exchanges will mint more USDC in their Circle accounts when they need more USDC to meet their users’ needs.

The Beginning and End of USDC Repegging

It all started with a run on Silicon Valley Bank, a California-based commercial bank founded in 1983, whose customers are primarily companies and individuals in the technology, life sciences, healthcare, private equity, venture capital and high-end wine industries, and is the 16th largest bank in the United States.

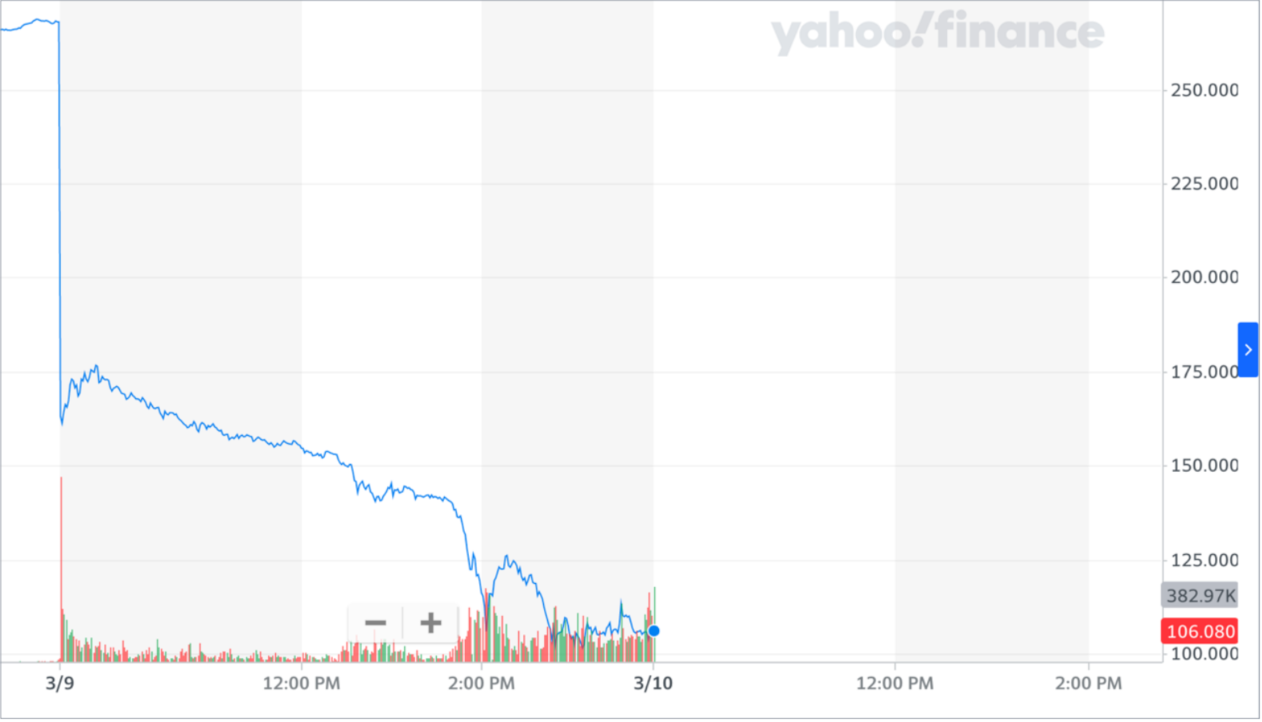

SVB’s total deposits tripled from $65 billion in 2019 to $189 billion in 2021, and its stock price rose from around $250 to a high of $750 with it. It was during this period that SVB invested its new deposits in long-term fixed income securities such as U.S. government bonds and mortgage-backed securities issued by U.S. government agencies. Starting in November 2021, the share prices of U.S. technology companies began to take a big dive, and many of SVB’s corporate users began to withdraw their deposits from SVB because of rising funding costs. And in response to inflation caused by the quantitative easing in 2020, the U.S. federal funds rate rises from 0.25% in March 2022 to 4.75% in February 2023. The rapid rise in interest rates means that the value of SVB’s low-yielding HTM securities holdings falls. To reduce further asset shrinkage, SVB began selling MBS and HTM at a loss. on March 8, SVB sold $21 billion worth of longterm Treasuries to Goldman Sachs, resulting in a $1.8 billion book loss. In response to a run-on demand from users, SVB sold $1.75 billions of shares. The run on SVB was further exacerbated by a 60% drop in its share price to $106 on March 9 from $267 on March 8. On March 10, SVB was taken over by the FDIC.

Source: https://finance.yahoo.com/

On March 11th, Circle tweeted that Circle had $3.3 billion in cash deposits on SVB, or roughly 7.5% of its total reserves, which quickly triggered panic in the market. As the off-chain redemption of USDC was limited by the operating hours of the US banking system, a large number of USDC holders chose to exchange USDC for other cryptocurrencies on-chain, causing USDC to begin to depeg from the US dollar, and within less than 15 hours, USDC fell as low as $0.87 on some DEXs. In response to the huge demand for USDC redemptions, Coinbase also reacted quickly by suspending the conversion of USDC to US. On March 12th, the US Treasury, Federal Reserve and FDIC issued a joint statement authorizing the FDIC to ensure that all depositors at Silicon Valley Bank would receive their full deposits starting on March 13th. Meanwhile, the market sentiment gradually calmed down and USDC gradually returned to $1.

Data source: coingecko.com

Impact of USDC Depeggingon Coinbase

Let’s imagine an extreme scenario: if the $3.3 billion Circle has deposited with SVB is completely unavailable for retrieval, how would Circle and Coinbase react to the risk of USDC de-pegging?

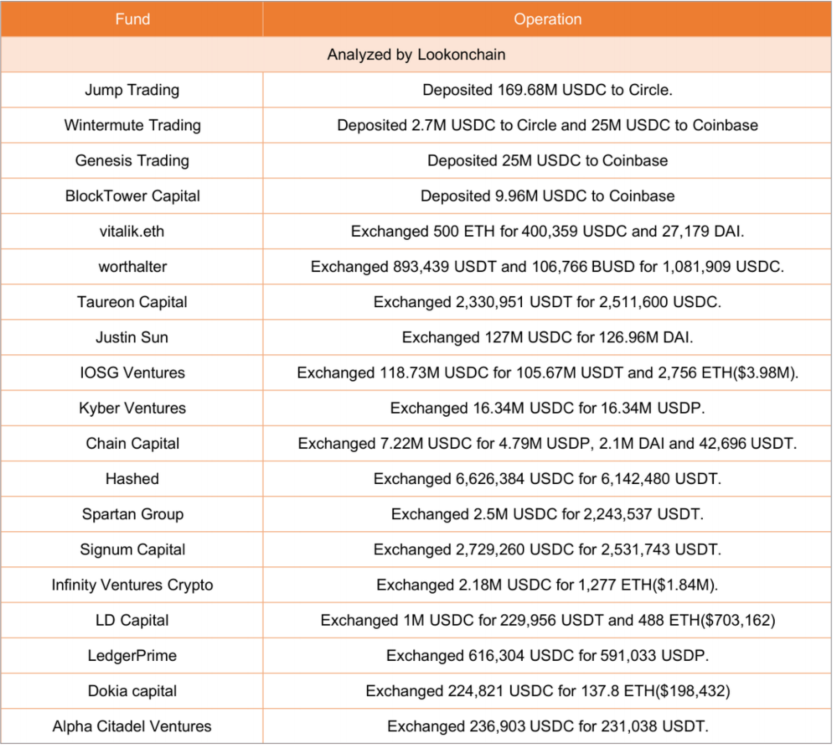

Back in March 11, the price of USDC started to depeg from $1 immediately after Circle published the information regarding to the deposit on SVB, since at the time people did not know whether Circle were able to retrieve its money from SVB in time, even though they knew that Circle has most of their reserves in short-term US treasuries. It is understandable that some of the largest crypto funds either exchanged USDC to other coins or tried to redeem USDC for USD in Circle and Coinbase to avoid the potential loss during the uncertain period.

Data resource: https://twitter.com/lookonchain/status/1634553237155217409

It was at such a critical time that Circle and Coinbase demonstrated their attitude and commitment to handling the crisis.

Known for its compliance and transparency, Circle has been updating USDC holders on its progress, and on March 11th Circle released a news release stating that it had $3.3 billion in cash deposits with SVB, and that despite initiating a transfer request for the funds on the 9th, the settlement was not completed by the 10th (Friday), while promising that if the FDIC is unable to pay out 100% to depositors, Circle will, if necessary, would use company resources to compensate losses to support USDC.

On March 13, Circle announced a new bank partner for minting and redemption (automatic settlement) of USDC, Cross River Bank, which is FDIC insured, and the 3.3 billion deposits transferred from SVB have been settled.

As of March 14, Circle has redeemed $2.9B USDC and minted $0.7B USDC. Most of the cash is held at Bank of New York Mellon, a small portion at a partner bank for USDC minting and redemption, and most of the reserves are invested in the Circle Reserve Fund, which is held in custody at Mellon Bank and managed by Blackrock. On March 15th, Circle released the news that Circle has completed all USDC minting and redemption requests.

Currently, Circle has 37.1 billion in USD reserves, of which USD 29 billion (78.2%) is in highly liquid short-term US Treasuries, held in custody at Bank of New York Mellon and managed by Blackrock, and USD 8.1 billion (21.8%) is in cash, which is held at various banks. The greatest risk to USDC is a complete collapse of its bank partners or default by the U.S. government, which is highly impossible, and even if there is a large number of USDC redemption requests, Circle can respond to the liquidity crisis by

selling short-term Treasuries.

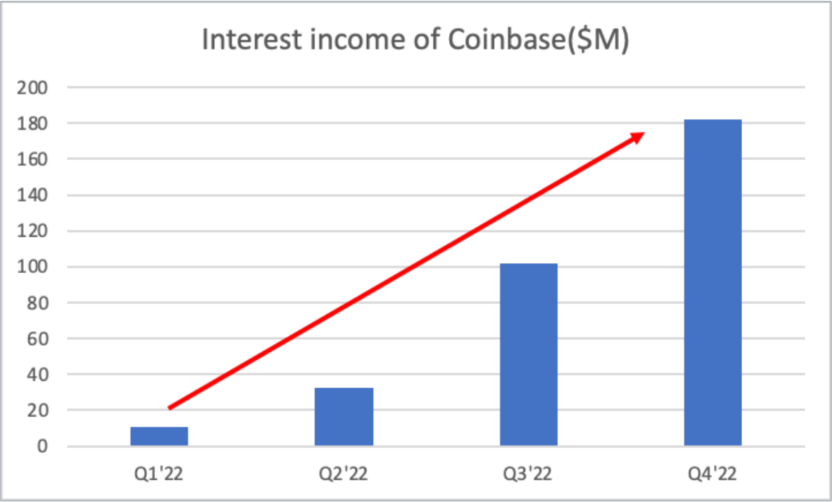

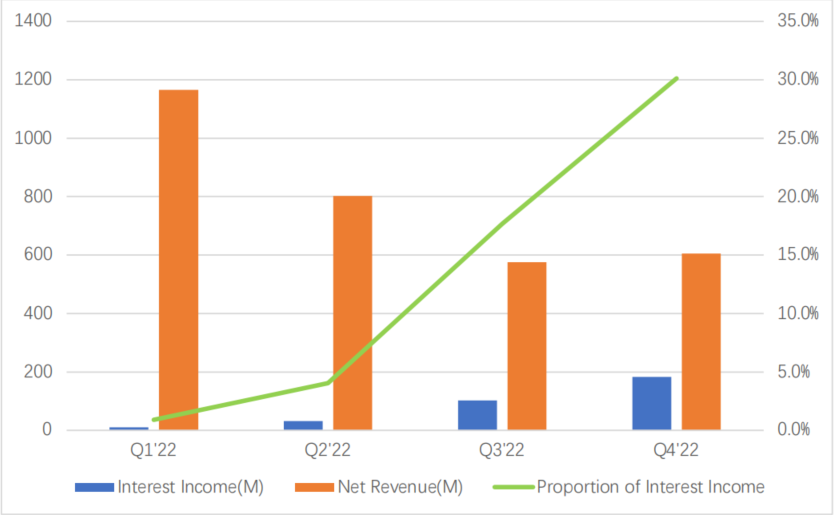

For Coinbase, as the first exchange to back USDC, it is apparently not going to sit idly by while USDC was depegging. It was recently announced that Coinbase had planned to put up $3 billion to help Circle through the crisis, but in the end the FDIC’s statement made Coinbase’s bailout unnecessary. Also, the interest income from USDC’s reserves is a big source of income for Coinbase. As you can see from the two charts below, while Coinbase’s net income fell in four consecutive quarters in 2022, interest income from USDC reserves has been rising, even reaching $18.22 billion in the fourth quarter of 2022, a 79% increase compared to the third quarter.

Coinbase’s Interest Incomein 2022, Data source: Coinbase Q4 Shareholder Letter

The Proportion of Coinbase’s Interest Income in 2022, Data source: Coinbase Q4 Shareholder Letter

Conclusion

USDC’s de-pegging was somewhat surprising, given the fact that USDC had been the top choice for people in the crypto market to hedge their bets until then. However, what needs to be made clear is that the root cause of this crisis is not something wrong with USDC or Circle itself, but a run-on of traditional banks. Circle’s response to the crisis has made the digital asset market realize that transparency and trust are the cornerstones of a stablecoin - people need to see that the stablecoin they have in their hands is readily convertible to USD. In some aspect, the re-pegging of USDC has somehow even raised the status of USDC in the long run, since the 100% reserve system and total transparency strategy adopted by Circle is easier to gain trust, compared to the fractional reserve system used by traditional banks. Although there is no doubt that numerous bumps ahead of us, we still believe that more people will benefit from a stablecoin like USDC, which has been providing users better financial services.